Liga Asuransi – The Internet of Things, where all the digital equipment we use is increasingly connected, has entered the daily lives of everyone in this world and changed business models across industries. This condition also brings opportunities to the insurance world: to develop new products, open new distribution channels, and expand their role to include prediction, prevention, and assistance.

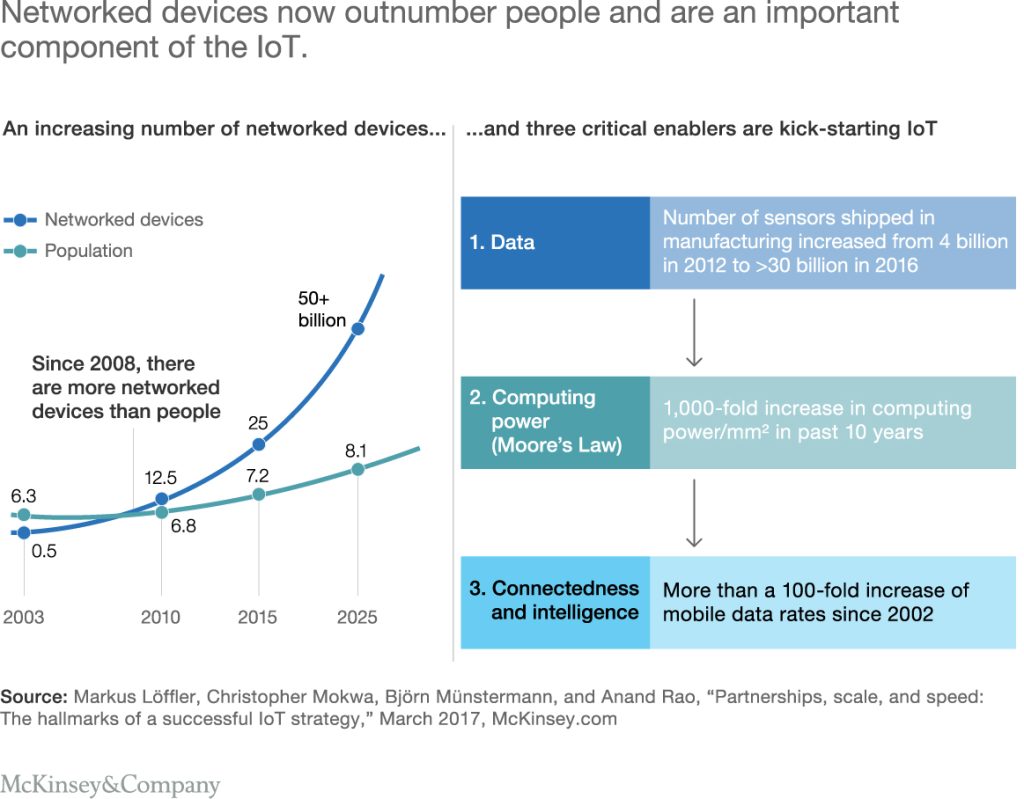

The Internet of Things (IoT) will radically change world conditions, especially in the coming years, because even now, we are starting to feel the change, and we inevitably have to be prepared to follow that change, where network devices will become an important part. In 2010, people owned 12.5 billion network devices; it is estimated that by 2025 this number will increase to more than 50 billion (Figure 1). People use digital devices, many of which are equipped with sensors and auto-launch functions, in almost all areas of their lives, including for work and leisure. It has long been possible to attach it quickly and easily and wear it anywhere on the body. These devices can transfer enormous volumes of data to providers or third parties—whether for real-time analysis or to trigger reactions or services automatically—and have transformed traditional business models and operations in many sectors.

The Hyundai car manufacturer is starting to incorporate IoT into its newest cars. The Hyundai Creta is equipped with sensors that can send a signal to the Call Center when an emergency occurs. With this sensor, the call center can quickly position obstacles to send assistance to the car’s insurance companies and can also adopt this technology in developing their services.

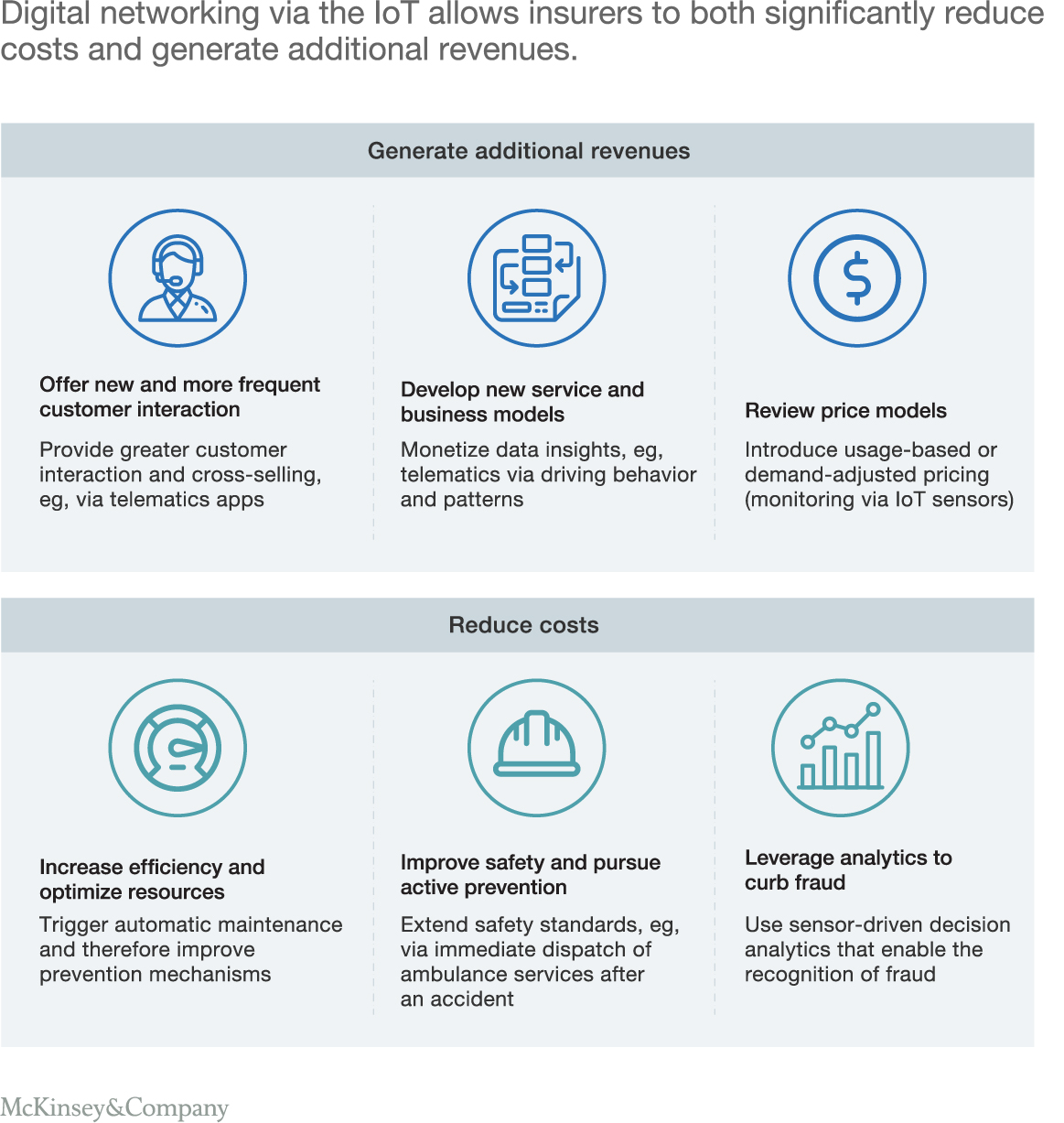

Insurers are using IoT capabilities to aid customer interaction and speed up and simplify underwriting and claims processes. Increasingly, insurance companies are developing interesting IoT-based services and business models. Digital networks through IoT can become a strategic component for insurance companies. Insurance companies can partner with companies to provide better cross-industry products and services, which are discussed further below (Figure 2).

IoT technology allows insurance companies to determine risk more precisely. Auto insurance companies, for example, have historically relied on indirect indicators, such as a driver’s age, address, and creditworthiness, when setting premiums. Now, data about driver behavior and vehicle usage, such as how fast the vehicle is driven and how often it is driven at night, is available. Applying such technology in countries where markets are much more mature means that insurers can assess risk more accurately in this way.

Network tools also allow insurers to interact more frequently with their customers and offer new services based on the data they have collected. Particularly in the insurance sector, customers often deal exclusively with agents or brokers; Direct contact with customers is limited to contract extensions and handling insurance claims. Therefore IoT can have considerable benefits for customer relationships, enabling companies to establish more intensive and targeted customer contacts.

So how can insurers develop attractive IoT offerings and successful strategies for setting up and engaging in an IoT-based ecosystem?

What digital ecosystems are most important to insurers

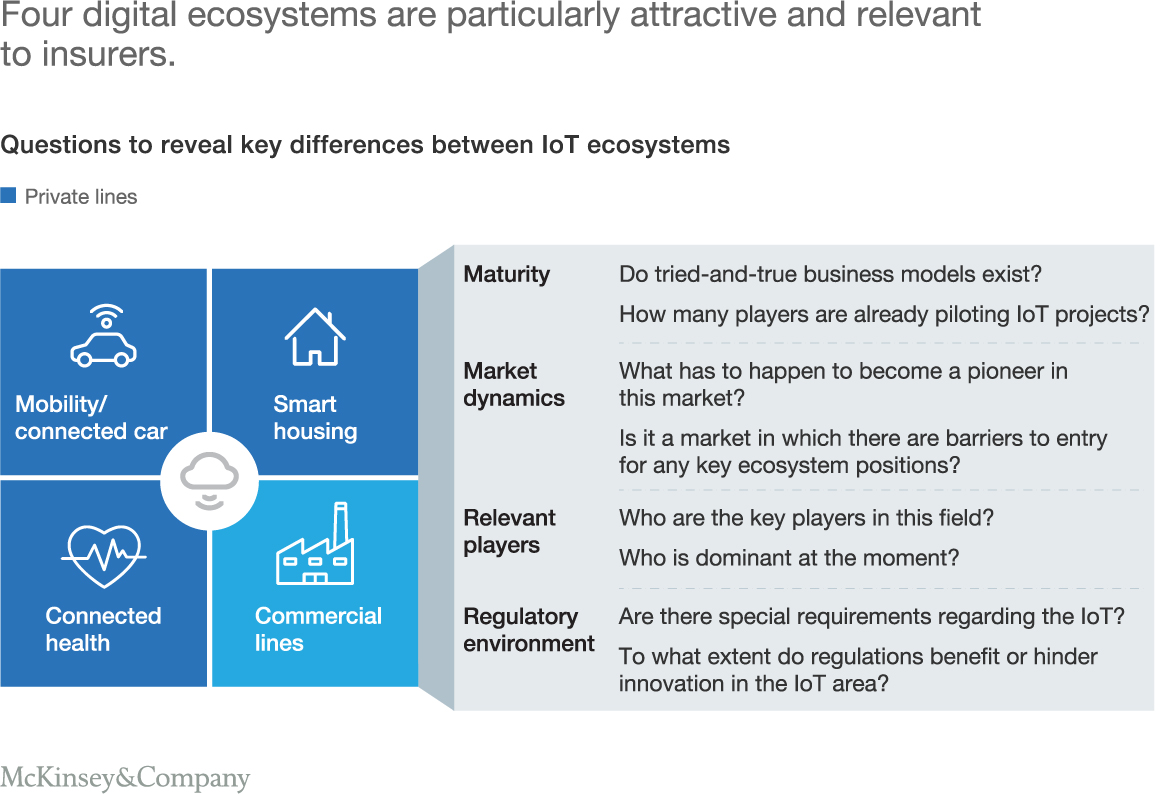

Four digital ecosystems are relevant and attractive to insurers: mobility/connected cars, innovative housing, connected health, and commercial lines (Exhibit 3). While these ecosystems certainly have parallels based on their basic dynamic measures, at a more detailed level, they have fundamental differences, which is why insurers need to develop specific strategies for each ecosystem. Market maturity levels differ across ecosystems and display distinct differences in market dynamics, relevant players, and regulatory environment.

The overarching dynamics can be explored using two examples: the mobility/connected car ecosystem, the most advanced of the four ecosystems, and intelligent housing, specifically Ambient Assisted Living, which combines smart homes and connected healthcare innovatively and effectively.

Mobility/connected car

The automotive industry and the mobility/connected car ecosystem demonstrate how digital ecosystems function and what dynamics of development they can reveal. It also illustrates the entrepreneurial opportunities and challenges of this new environment.

Cars—and their drivers, if they carry smartphones—are increasingly equipped with sensors that monitor driving behavior and vehicle use and collect other vehicle data, from oil temperature and brake wear to tire pressure. This data forms the basis for countless new applications contributing to customer convenience and active and passive security. This kind of app enhancement is creating a whole new ecosystem around connected cars, not just covering automotive OEMs. Other players in this landscape include telecom operators, sensor and chip manufacturers, digital platform operators such as Uber, research institutes, standardization centers, and insurance companies.

This ecosystem changes the competitive parameters for all participants, particularly insurance companies. While the frequency of network vehicle claims will decrease, the abundance of sensors on and in the car will increase the average number of shares due to the high cost of repairs. Even if high-risk customers can be distinguished from low-risk ones by using additional data from the new ecosystem, the overall premium may fall due to the discounts offered for telematics usage. While conscientious drivers can justifiably expect a sizable reduction in their insurance premiums, insurers likely will only be able to compensate for this decrease by increasing rates for high-risk drivers.

Fighting fraud more effectively, increasing the use of allied repair shops, and offering assistance and other services are all initiatives that have the potential to more than offset reduced premiums. Insurance companies need to look for other triggers for reducing claims expenses through optimized risk selection to minimize the impact of the resulting reduction in premiums. Insurance companies could, for example, provide services to avoid risks, show drivers necessary maintenance work, and identify intelligent parking solutions. Insurers may also sell their data and analytics solutions to third parties, such as media agencies focusing on location-based advertising.

Insurance companies worldwide have partnered with IoT-based telematics suppliers, automotive OEMs, auto repair shops, telcos, and system operators who guide drivers to clear parking spaces. Such a partnership will give both parties access to valuable sensor data that will lay the groundwork for a new hybrid insurance model.

However, this partner may have a better and more intensive relationship with the insurance customer than with the insurance company itself. Companies outside the insurance industry are also increasingly generating risk-related data, and many have the necessary skills to draw relevant conclusions. In other words, while insurers may unlock massive value from new IoT-based ecosystems, players in other sectors may be closer to the customer interface.

Smart housing and smart health

The insurance market did not embrace smart housing at first—mainly because the potential for new markets was too limited for technical reasons and the solutions available in the market were slow to meet technical standards.

In recent years, the mass market has opened up by facilitating simple connections with more and more devices. However, this situation has changed as technology has matured rapidly. With the rise of Google, Amazon and other providers are putting their smart home offerings on the market. As a result, many insurance companies worldwide (for example, Allianz) have embarked on a partnership model, selling integrated products through Google Nest or offering insurance discounts for people who equip their homes with smart home devices. In addition, these insurance companies provide digital add-on services such as home security and convenience services (e.g., Liberty Mutual).

Customers expect more and different services from insurance companies. Most smart home insurance products fall under the property and casualty insurance market segments. Insurers have treated the product as new, more modern home contents and add-in insurance, despite developing additional services and pricing models. As insurance companies continue to sell traditional products, it is evident that new customer segments can be addressed with smart home insurance products.

An extension of smart housing is Ambient Assisted Living. This field is also linked to connected healthcare, which is especially relevant in aging societies in industrialized countries. People with reduced mobility, for example, are increasingly looking for innovative services to assist with their daily activities and enable them to live an independent lifestyle at home. Potential customers from this segment are likely to have a positive attitude towards IoT and related technologies, as well as towards insurance companies acting as the leading providers of this kind of new service package. Insurers can take advantage of opportunities in this sector by providing customers with additional services that allow insurance companies to minimize costs. Insurers can also position themselves as digital coordinators of care services and providers such as protects and general and specialized housing associations.

Commercial / Business Areas

One area of high value at stake is commercial ecosystems—that is, ecosystems centered on distributing to business partners (B2B or B2B2C) and leveraging partnerships along the value chain. Whereas private line ecosystems aim primarily at optimizing customer touchpoints, commercial ecosystems often focus on data and operational excellence.

Insurance companies in the business/corporate sector have various ecosystem games along the value chain: product innovation, distribution excellence, risk prevention, holistic service provision, supply network management, and capital-to-risk matching. An example of product innovation involves Cyber Risk Security (Cyber Risk Insurance) because it is only through additional risk management and assistance services that it is possible to ascertain cyber risks—hence the emergence of new partnerships between insurers and providers of cyber security software and hardware IoT. IoT-enabled risk prevention could include, for example, sensors in a warehouse to assess risk—and therefore price—at a more granular level. Supplier network management has been frequently applied in motor vehicle (fleet) insurance for garages and director’s and officers’ liability insurance for attorneys. And capital-to-risk matching refers to electronic platforms for trading new forms of insurance-related securities—allowing insurers to transfer risk through markets, as some commercial line insurers already do.

IoT in daily work in the field of insurance

The Internet of Things can not only be used to expand the business of an insurance company or insurance broker. But Iot can also be utilized by all personnel/employees.

Before getting used to employees working with IoT, the company must first prepare a platform or tools that support it besides the mobile devices already owned by most employees.

With IoT, it becomes easier for sales to prepare presentation materials for clients because all data is available online on the platform designed by the company, so simply by accessing the data using a laptop or smartphone, the material can be downloaded more quickly and presented to clients. And can also upload that data for validation and approval. So that with this IoT can speed up and simplify the process of issuing a policy.